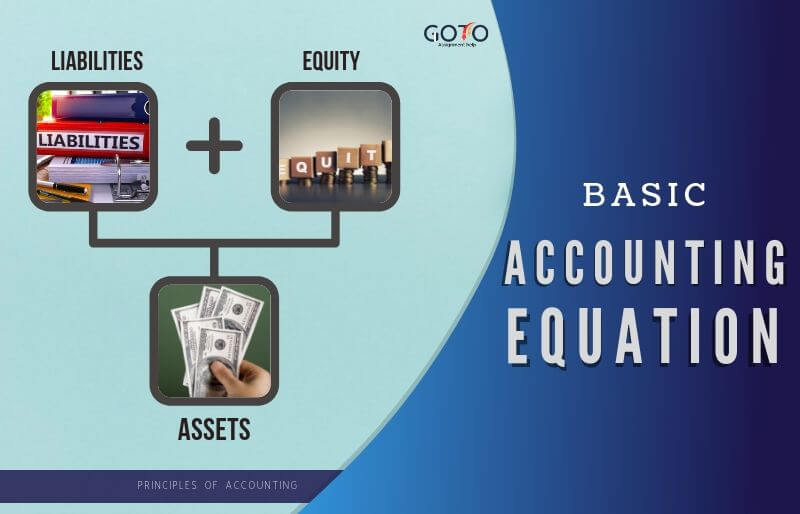

When the total assets of a business increase, then its total liabilities or owner’s equity also increase. The accounting equation ensures that a company’s balance sheet remains balanced. The equation is generally written with liabilities appearing before owner’s equity because creditors usually have to be repaid before investors in a bankruptcy. In this sense, the liabilities are considered more current than the equity. This is consistent with financial reporting where current assets and liabilities are always reported before long-term assets and liabilities. The shareholders’ equity number is a company’s total assets minus its total liabilities.

Financial statements

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources. 11 Financial is a registered investment adviser located in Lufkin, Texas. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements.

What are assets?

Shareholders’ equity is the total value of the company expressed in dollars. Put another way, it is the amount that would remain if the company liquidated all of its assets and paid off all of its debts. The remainder is the shareholders’ equity, which would be returned to them. 27 best freelance zapier developers for hire in february 2021 The accounting equation matters because keeping track of each transaction’s corresponding entry on each side is essential for keeping records accurate. To illustrate how the accounting equation works, let us analyze the transactions of a fictitious corporation, First Shop, Inc.

Components of the Accounting Equation FAQs

The balance is maintained because every business transaction affects at least two of a company’s accounts. For example, when a company borrows money from a bank, the company’s assets will increase and its liabilities will increase by the same amount. When a company purchases inventory for cash, one asset will increase and one asset will decrease. Because there are two or more accounts affected by every transaction, the accounting system is referred to as the double-entry accounting or bookkeeping system. The accounting equation is the backbone of the accounting and reporting system.

Think of liabilities as obligations — the company has an obligation to make payments on loans or mortgages or they risk damage to their credit and business. Assets typically hold positive economic value and can be liquified (turned into cash) in the future. Some assets are less liquid than others, making them harder to convert to cash. For instance, inventory is very liquid — the company can quickly sell it for money. Real estate, though, is less liquid — selling land or buildings for cash is time-consuming and can be difficult, depending on the market.

- Under the accrual basis of accounting, expenses are matched with revenues on the income statement when the expenses expire or title has transferred to the buyer, rather than at the time when expenses are paid.

- Often, more than one element of the accounting equation is impacted but sometimes, like with transaction 3, the same part of the equation (in this case assets) goes up and down, making it look like nothing has happened.

- This refers to the owner’s interest in the business or their claims on assets after all liabilities are subtracted.

- He forms Speakers, Inc. and contributes $100,000 to the company in exchange for all of its newly issued shares.

- Simply put, the rationale is that the assets belonging to a company must have been funded somehow, i.e. the money used to purchase the assets did not just appear out of thin air to state the obvious.

For example, you can talk about a time you balanced the books for a friend or family member’s small business. Capital essentially represents how much the owners have invested into the business along with any accumulated retained profits or losses. The capital would ultimately belong to you as the business owner. If an accounting equation does not balance, it means that the accounting transactions are not properly recorded.

Like the accounting equation, it shows that a company’s total amount of assets equals the total amount of liabilities plus owner’s (or stockholders’) equity. Income and expenses relate to the entity’s financial performance. Individual transactions which result in income and expenses being recorded will ultimately result in a profit or loss for the period.

Conversely, a partnership is a business owned by more than one person, with its equity consisting of a separate capital account for each partner. Finally, a corporation is a very common entity form, with its ownership interest being represented by divisible units of ownership called shares of stock. Corporate shares are easily transferable, with the current holder(s) of the stock being the owners. Earnings give rise to increases in retained earnings, while dividends (and losses) cause decreases. If a company keeps accurate records using the double-entry system, the accounting equation will always be “in balance,” meaning the left side of the equation will be equal to the right side.

This business transaction increases company cash and increases equity by the same amount. A liability, in its simplest terms, is an amount of money owed to another person or organization. Said a different way, liabilities are creditors’ claims on company assets because this is the amount of assets creditors would own if the company liquidated. Now that we have a basic understanding of the equation, let’s take a look at each accounting equation component starting with the assets.